One of the most successful corporate structures for long-term shareholder returns has been an insurer whose float is invested by a capable capital allocator. While Warren Buffett's Berkshire Hathaway (BRK.B) is the largest and best-known example, its success has been matched at a smaller scale by companies like Markel (MKL) and Alleghany (Y). Buffett explains the benefits of float in his 2009 annual letter:

If premiums exceed the total of expenses and eventual losses, we register an underwriting profit that adds to the investment income produced from the float. This combination allows us to enjoy the use of free money �� and, better yet, get paid for holding it.

In other words, the company gets to invest the insurance premiums paid by policy holders, providing a source of capital. The combination of profitable underwriting and even average investment returns can lead to the massive compounding of capital.

Profits are by no means guaranteed, however. Poor underwriting can lead to losses of float, as can poor investment of the float. Insurance float functionally adds leverage to the capital of an insurer and small insurers can be especially sensitive to unexpected insurance payouts. This risk played out recently in the 2017 hurricane season that exposed insurers in the Caribbean and Puerto Rico to tens of billions in insured losses.

Nevertheless, the desirability of a permanent capital vehicle has led to the creation of insurance companies by hedge fund managers, including David Einhorn with Greenlight Re.

Company Overview

Greenlight Re (GLRE) is a specialty property and casualty reinsurer with an A- A.M. Best rating. Einhorn, through DME Advisors, manages the investment portfolio of Greenlight Re with a hedge fund fee structure of 1.5% of assets and 20% of profits (with a loss carry forward provision that we will discuss the relevance of below). Greenlight Re does business in diverse lines of specialty reinsurance with heavy exposure to the U.S. auto insurance market.

Greenlight Re's insurance business operates in diverse lines out of two subsidiaries: one with a global focus in property, casualty, and various specialty lines operating out of the Cayman Islands and another writing property and casualty lines in Europe. Despite the broad mandate of its insurance business, Greenlight Re's underwriting business has been concentrated (>75%) in the U.S. and Caribbean over the past 3 years, and about 50% of gross premiums were derived from motor property and casualty lines.

The stock is a massive underperformer relative to the S&P 500 (SPY) in recent years with a loss in value of 11.8% in 2017 and 23.9% year-to-date. However, the insurance portion of the business appears to be improving with a combined ratio of 98.3% for the quarter ending March 31st, 2018. The biggest driver of Greenlight Re's recent negative performance is not its underwriting or a lack of capital to invest but its investment management by Einhorn and DME. Greenlight Capital, Einhorn's hedge fund proper, has experienced outflows of $3 billion over the last two years.

Poor Investment Portfolio Performance in 2017 and 2018

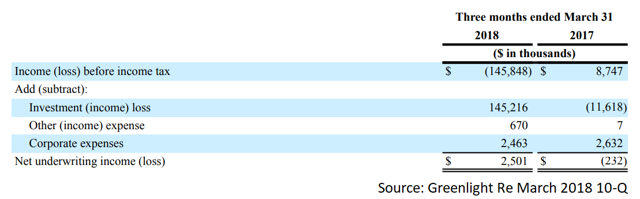

The book value of Greenlight Re fell to $18.35 per share as of March 31st, 2018, which represents a loss of 17.4% on the quarter and 22.1% on the year. While book value is not always indicative of true company value in many cases, its growth is how Greenlight Re itself measures its performance. This loss, however, is not attributable to the insurance underwriting business of Greenlight Re. Greenlight underwriting profits were $2.5 million in the first three months of 2018:

As you can see, the losses posted by Greenlight Re are fully attributable to its investment portfolio, which lost $145 million net of fees and expenses in this same period. These losses continued in April with another 0.5% detraction to the investment portfolio.

Einhorn is known for his long-short investing strategy, which led to marked outperformance during the last financial crisis. However, his recent performance, particularly in the last year, have been dismal compared to the overall market. In these three months, total losses in Greenlight Re's investments were 11.8% with the long and short portions of the portfolio contributing about equally to these losses. These results follow a tepid 0.9% net investment return for the 2017 calendar year while the S&P 500 (SPY) returned over 21%.

The biggest contributors to these declines were a short position in Netflix (NFLX), which gained 54% in the first quarter of 2018, and a long position in General Motors (GM), which lost 10%. Einhorn has been especially bearish the past few years on many high-flying tech names such as Netflix (NFLX) and Tesla (TSLA), which he shorts as part of his so-called "bubble basket".

An Opportunity to Invest Alongside an Underperforming Manager

Academic research has shown that managers that have underperformed over the past 3 and 5 year periods end up overperforming in the subsequent 3 and 5 year periods, what can be explained as a form of mean reversion in the best performing investment strategy. David Einhorn, with his long-short strategy, has been a perennial underperformer relative to the S&P 500 (SPY) since 2008/2009 where his portfolio strategy provided a buffer against the large losses posted during the last financial crisis. If you share an investment thesis with Einhorn, then investing in Greenlight Re could act as a hedge on the froth in the market, particularly in the technology sector.

So what is currently in Greenlight Re's portfolio?

As of December 2017, Greenlight Re's major (10%+) long positions were General Motors (GM), Brighthouse Financial (BHF), gold (GLD), Bayer (OTCPK:BAYZF), and Mylan (MYL). It also holds a long position in Micron (MU), which was the best positive contributor to its portfolio in the first quarter of 2018. These long positions were balanced by shorts in Tesla (TSLA), Netflix (NFLX), and other "bubble basket" stocks. The portfolio is also short Assured Guaranty (AGO), a municipal bond insurer, a position which is hedged by a simultaneous long in Puerto Rican debt. Overall, the portfolio is 93% gross long and 65% gross short. Unlike most insurance portfolios, just 0.5% of investments are in debt instruments and, in fact, Greenlight Re's short portfolio was 11% allocated to sovereign debt.

The long portfolio has a significant value-tilt. General Motors (GM), Brighthouse (BHF), and Mylan (MYL) all have forward P/E ratios < 7 and free cash flow yields > 10%. The short portfolio is comprised mainly of high growth names and other individual theses that Einhorn holds. Assured Guaranty (AGO) is not a growth stock but is shorted by Einhorn on his view that it lacks the financial strength to overcome its exposure to municipal debt, particularly that of Illinois and Puerto Rico.

Despite the fees charged to the investment portfolio, investing with Einhorn through Greenlight Re may be a compelling opportunity. The portfolio is not just randomly long-short but tries to take advantage of specific opportunities rather than simply being hedged to the fluctuations of the market. You get the benefit of exposure to the investment research of a hedge fund with a portfolio that is unlikely to be correlated with the overall market. If you generally agree with Einhorn's investment strategy or would like exposure to a long-short portfolio, Greenlight Re could act as a replacement to a pure investment in a hedge fund.

A further incentive to invest now is the discount to book value, which is currently 17%. The company itself recognizes this disparity between book and share price and has recommitted to a share repurchase program, which may help to narrow this gap in the short- to medium-term. As noted above, Greenlight Re has a loss carry forward provision with Einhorn and DME Advisors. The agreement is structured such that the 20% performance fee on net profits is reduced to 10% until 250% of the loss is recouped. Combined, a purchase at current prices (< $15.5 per share) gives a significant discount to exposure to Greenlight Re's investment portfolio and to a functional fee discount on potential future portfolio returns. Greenlight Re can be comfortably held in a taxable account as it currently pays no dividends.

Is the Insurance Vehicle a Boon or a Bane?

Buffett's deployment of insurance float to great success depended on the profitability of his underwriting business, and has lowered his exposure to reinsurance. In his 2017 annual letter, he warns on the long-tailed losses possible in property and casualty insurance that may not become apparent for many years. In this regard, Greenlight Re is relatively shielded from catastrophic losses as it largely exposed to shorter term policies such as motor liability. But, just how good is Greenlight Re's insurance business, to which an investor in the common stock of GLRE must be exposed in order to "access" Einhorn?

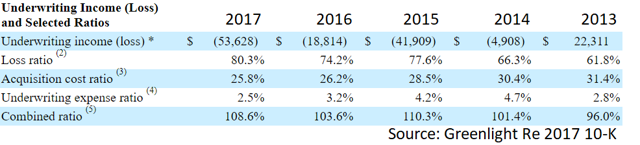

Because Greenlight Re's policies are generally short term, underwriting profits (and losses) should be reflected quickly in their financials. Unfortunately, despite profitability in the first quarter of this year, the past four fiscal years have all recorded underwriting losses and combined ratios greater than 100%:

If Greenlight Re is losing money as it tries to generate float, an investment in the common at a book value discount may actually be a mark of market efficiency rather. However, if you believe that the most recent results and efforts on higher quality and more profitable underwriting described in Greenlight Re's last conference call, then perhaps the discount is unwarranted. Greenlight Re has recently entered into new insurance markets in London, an area where its executives claim they have particular expertise.

On a positive note, unlike many larger insurers that are struggling to profitably invest their float in a low yield environment, Greenlight Re is unrestricted in its investments and has practically no exposure to fixed income beyond cash equivalents. You are, in fact, getting significant exposure to Einhorn's investment strategy if Greenlight Re can continue to shore up its underwriting business.

Conclusion

Greenlight Re is an opportunity to invest in a permanent capital vehicle alongside David Einhorn that appears to be improving its underwriting business. The stock gives combined exposure to the reinsurance business and a long-short hedge fund portfolio at a discount to book value with heavy exposure to value.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in GLRE over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment